Main points:

- All models are wrong, some models are useful

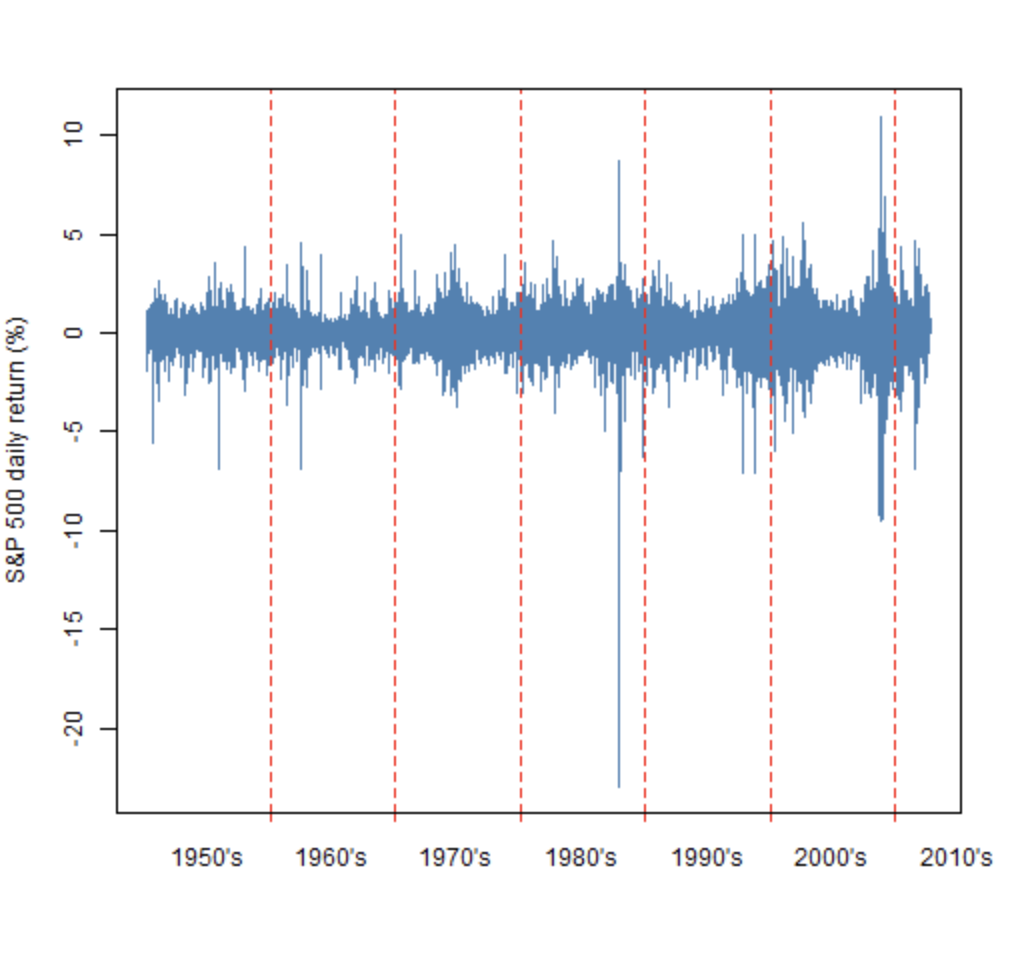

- garch is a model of volatility clustering

- garch is impacted by the 3 realms of finance, statistics and computing

- garch is data hungry

- variance targeting seems to be useful

- there is at least one model that is better than the garch(1,1)

- R is a good environment for academic research if you want to have real impact

Presented 2012 December at the Imperial College Algorithmic Trading Conference.

Kommentarer inaktiverade för 3 realms of garch modelling

maj 22, 26

I recently gave a talk at the R in Finance conference in which I introduced the marketAgent package for R. I’ll be giving more details of the talk real soon now.

maj 22, 26

I recently gave a talk at the R in Finance conference in which I introduced the marketAgent package for R. I’ll be giving more details of the talk real soon now.

maj 22, 26

I recently gave a talk at the R in Finance conference in which I introduced the marketAgent package for R. I’ll be giving more details of the talk real soon now.